hanimmal

Well-Known Member

https://apnews.com/article/business-economy-f0ff47ba21bbf4580cf9366d67a213d2

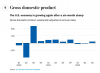

WASHINGTON (AP) — Shrugging off rampant inflation and rising interest rates, the U.S. economy grew at an unexpectedly strong 3.2% annual pace from July through September, the government reported Thursday in a healthy upgrade from its earlier estimate of third-quarter growth.

The rise in gross domestic product — the economy’s output in goods and services — marked a return to growth after consecutive drops in the January-March and April-June periods.

Still, many economists expect the economy to slow and probably slip into recession next year under the pressure of higher interest rates being engineered by the Federal Reserve to combat inflation that earlier this year reached heights not seen since the early 1980s.

Driving the third-quarter growth were strong exports and healthy consumer spending.

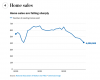

Investment in housing plunged at an annual rate of 27.1%, hammered by higher mortgage rates arising from the Fed’s decision to raise its own benchmark rate seven times this year.

Thursday’s GDP report was the Commerce Department’s third and final look at the July-September quarter. The first look at the fourth quarter comes out Jan. 26. Forecasters surveyed by the Federal Reserve Bank of Philadelphia expect the economy to grow again the last three months of the year — but at a slower, 1% annual rate.

In its previous estimate of third-quarter growth, issued Nov. 30, the Commerce Department had pegged July-September growth at an annual rate of 2.9%. Behind the upgrade to Thursday’s 3.2% was stronger growth in consumer spending, revised up to a 2.3% annual rate from 1.7% in the November estimate.

“Despite a rapid increase in interest rates, the economy is growing and importantly, households are still spending,″ Rubeela Farooqi, chief U.S. economist at High Frequency Economics, said in a research note. “However, looking ahead, in 2023, we expect a slower growth trajectory.″

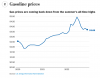

Inflation, which had not been a serious problem for four decades, returned in the spring of 2021. It was set off by an unexpectedly strong recovery from the coronavirus recession of 2020, fueled by massive government stimulus. The Fed was slow to recognize the severity of the inflation problem and only began raising rates aggressively in March.

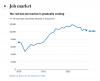

The job market has stayed resilient throughout, putting upward pressure on wages and prices. Employers have added 392,000 jobs a month so far this year, and the unemployment rate is at 3.7%, just off a half-century low.